Reflections after a decade of pursuing Financial Independence (FI)

Reflections after a decade of pursuing Financial Independence (FI)

Our co-founder Ruiming looks back on his hustling days from 2014. DISCLAIMER: THIS IS AN EMAIL NEWSLETTER EXCLUSIVE BROUGHT TO YOU BY THE WOKE SALARYMAN.

Ten years ago, my mom had a stroke, which ignited my journey to financial independence.

It was quite a different time.

The personal finance landscape in Singapore was quite different. Content creators in this space were few and far between. The Woke Salaryman did not exist yet. Not till 2019, at least.

HDB flats prices were actually on the decline. The first high-yield savings account, OCBC 360, just launched. Inflation was 1%. Even LKY was still alive.

In 2014, 25-year-old RM earned $2,700 as a junior copywriter, worked about 10–12 hours a day, and was looking for a way out of the proverbial rat race.

In his mind, he settled on a few things:

1. Save his first $100,000 — and invest at 4% p.a to earn $4,000 returns a year. Use that to stop working for a month. He wanted to reach this at 30 years old — based on this 2013 article.

2. Repeat the feat five times to save $500,000 by the time he was 35. Then he would be financially comfortable enough to achieve Barista or Coast FIRE.

3. This meant earning $20,000 in passive income, allowing him to take on a less stressful role, while still being able to live like a regular adult; owning his own place, paying his own bills etc. If he wanted to, he’d also be able to take six months off each year for travel, and work the other six as a freelance copywriter.

Well, I’m 35 years old this year. And I have a lot to thank 25-year-old RM for.

Say what you will, but the dude was committed to the goal. He was forward-thinking and disciplined as hell. In fact, he’d be proud of a lot of the things I’ve accomplished since 2014.

But he also didn’t foresee quite a lot of things that happened along the way.

This article is about those things.

His financial goals were affected by inflation

$20,000 is still quite a substantial amount for passive income in 2024, but it's not quite what it used to be after COVID-19 and the rapid inflation that followed.

Housing is probably the most obvious example of this. $20,000 annually is $1,600 a month; enough for a co-living space without an ensuite toilet. But not enough for an entire place with privacy.

If we’re talking about owning a place, the median HDB price rose from $426,000 in 2014 to $575,000 in 2024. 2014-RM would be able to buy a place and be debt-free for sure. But he’d still be a long way off from financial freedom.

In some ways, my plans in 2014 were affected by the recency bias. Inflation in Singapore was slow and steady for a long time, and I had expected it to stay this way.

He had different ideas of work and retirement

25-year-old RM did not dream of labour. He saw work as a dreadful thing and hoped to escape it. He enjoyed few aspects of his work and did not find work purposeful. He was disillusioned with corporate structure, and organisations that were crippled with inefficiencies and idiosyncrasies.

Even when he got subsequent pay bumps, this attitude did not change. The increase of money was welcomed, of course. But only because it sped up his journey towards financial independence.

But eventually, being able to leverage my skills from advertising/content marketing with my knowledge of personal finance, economics and investing allowed me to start this blog with Wei Choon. Being in good stead financially also gave me the opportunity to start a company that was more aligned with my values; and eventually build a team I genuinely enjoy working with.

These days, I find work meaningful because I work for purpose instead of money. And my colleagues are fun to hang out with. On long travels, I actually get restless if I don’t write or create content.

I’m 35 now, and I don’t think I’ll ever stop working. Even when The Woke Salaryman shuts down eventually, I’d use my financial freedom to look for something else to work on.

He did not expect some side hustles to go away (so soon)

In the 2010s, you could make quite a decent amount of money as a freelance copywriter, or a feature writer.

This is no longer the case; the advertising industry has changed so much that there’s no longer constant demand for freelance copywriters.

It is the same with things like video editing, transcribing or SEO writing — thanks to Generative AI and the increasing skill set of labour from developing countries.

Yes, side hustles still exist for Singaporeans these days. But a lot of them do need specialised or localised knowledge.

Which prompts the question: What will things look like in the next 10 years?

He — like many others — was laughably obsessed with the small stuff

One of the most enduring myths about personal finance is that to be ‘good at personal finance’, you need to master things like:

Which credit card gives you the best miles

What are current interest rates for treasury bills

What is the year-to-date return of the S&P 500

Which bank gives the highest interest rates

It’s not that these aren’t useful. But they’re more tactics than strategies. Tactics are small pictures. Strategies are big picture stuff.

The problem is that a lot of people can be good at tactics, but are shit at wealth-building strategies. Being overly focused on tactics is like winning the battle but losing the war.

For example: Someone can be an expert at which credit cards give the most miles. But as a result, they spend beyond their means and go into debt to achieve those miles.

From my experience, the things with the highest ROI when it came to personal finance were these:

Strategy: Earn more income

Corresponding Tactics (Examples):

Negotiating higher salary

Working on soft skills

Finding out which are in-demand industries

Developing a USP

Strategy: Invest consistently without catastrophic risk

Automating investments to take out the guesswork

Limiting exposure to high risk investments (5-10%)

Investing in low-cost passive index funds

Diversification across companies, asset class and geographies

Strategy: Live below your means

Maintain reasonable spending even when you start becoming a high earner

Never spend more than 1% of your net worth on rent

Following the 3-3-5 rule when it comes to housing

Further reading: The Single Mistake Everyone Makes In Their 20s Trying To Build Wealth

He didn’t expect financial freedom to be lonely (well, kinda)

25-year-old RM assumed that having financial freedom would give him the ability to do anything he wanted. He could fly whenever he wanted, buy whatever he wanted.

It would basically solve all his problems.

After my first $300,000, I already knew that things like mental health and physical health were important. But, the social implications of being financially free did not hit me till the start of 2023 — when Wei Choon and I went on a cycling trip around Taiwan.

We counted less than five of our mutual friends who could join us for the trip.

My realisation is that while you might achieve financial freedom, the people that you might actually want to hang out with might not. That limits the activities you can enjoy together.

That’s not to say financial freedom is not worth pursuing. I am grateful for achieving it. That said, you shouldn’t expect it to be a magic bullet.

Money is great; and it’s a great tool for your goals. But don’t expect to instantly transform money into authentic relationships or a healthy body. That takes time and effort.

Here’s my little secret to staying focused and not getting discouraged

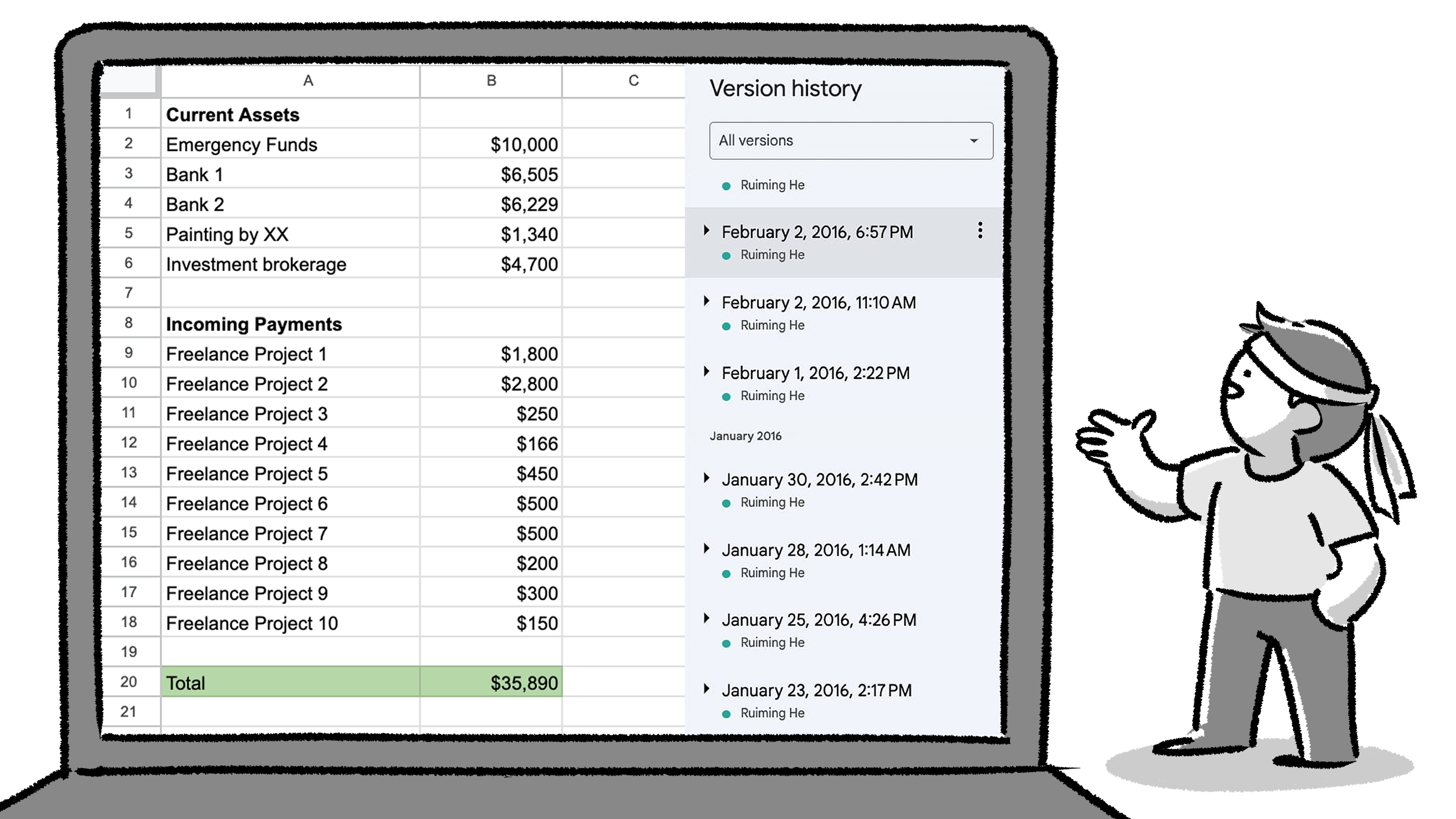

One thing I really appreciate about 25-year-old RM is that he started a Net Worth tracker on Google Sheets at the start of 2016. Since then, I’ve updated it at least fortnightly to update the state of my finances.

(We made a copy-able version of this sheet that you can use to track your net worth too.)

This has been invaluable in my FI journey. But not because I think tracking expenses is the holy grail of personal finance.

Hear me out:

There were times in my FI journey when I felt discouraged. In 2017, I had multiple personal emergencies that took a big chunk out of my net worth. In 2021, I lost six-digits from my net worth from investing in crypto when the markets tanked.

I took these setbacks hard.

But each time, I could also scroll through past document versions to remind myself of how far I’ve come.

Reminding myself that I’ve reached the goals that 25-year-old RM once dreamt of made me feel a little better.

A parting word

If you just so happen to be a young 25-year-old reading this, I'm pretty sure your journey over the past 10 years won't be exactly the same as mine.

We are, after all, products of our time — and your journey will most certainly be affected by world events that have yet to unfold. These can make or break your financial plan.

Case in point: If I was born 5 years earlier, or 5 years later, things could have looked very different.

I was fortunate to have started my journey in the 2014s; the world had recovered from the 2009 Global Financial Crisis, social media was new, and I was able to use my millennial-ness to become a first mover in what turned out to be quite a lucrative field. Stock markets didn’t perform too shabbily either.

And as you read this, the next crippling crisis is probably on its way to us. A pandemic; a world war; a major economy mismanaging its finances — whatever it is, unstoppable wheels are already in motion. The writing is already on the wall.

That said, there are timeless principles you can look to. Working on your earning power. Living below your means. Understanding what money can, or cannot, buy. Making use of the good times, so you can remain calm during the bad ones.

In the grand scheme of things, these are the only things we can do.

The rest of it? It’s up to time itself.

Stay woke, salaryman.

If you’ve read this far, please consider subscribing to our email newsletter (yes, this Substack). We cannot offer you much but we can offer this:

We have newsletter-exclusive articles that won’t be posted anywhere else. We created these articles for people who want to go deeper into complex issues than the shorter-form content we typically have.

If you don’t have social media or don’t follow our Telegram channel, you can still get updates to all our content emailed directly to your inbox to read at your own time.

We promise not to spam your inbox (but Substack might, so update your notification settings).

thank you for sharing your insights. posting online can feel like talking to an empty void, yet i just wanna say that your generosity is influencing people like me, an 18 yr old.

Awesome!