What we think about the controversial CPF-SA change

ICYMI: Starting 2025, the CPF Special Account will be closed for people 55 years old and above.

Changes were made to CPF, and not everyone is happy. Namely, Singaporeans who have a significant amount of money – above the Full Retirement Sum (FRS) – in their CPF.

What they are unhappy about: The end of the CPF Shielding Hack

Previously, Singaporeans at 55 had access to their CPF Special Account (SA) which gave them 4% p.a., and that you could withdraw from anytime — kinda like a high yield savings account.

Eventually a group of very ingenious people found a way to use this to their advantage, and it’s been called the “CPF Shielding” hack.

You can read more about CPF Shielding here.

Essentially, the hack would allow you to earn more interest on your CPF monies by keeping most of them in your SA (earning 4% interest), instead of your OA (earning 2.5% interest).

The difference in interest earned can be quite significant, if you see the table below:

Why we are ambivalent:

Reason 1: We’ve always seen CPF as something to provide for your basic retirement needs.

The word here is basic. This includes expenses like food, utilities, mortgage (if you still have), even the occasional holiday or two, but nothing premium.

The change doesn’t affect Singaporeans who don’t have or just have the Full Retirement Sum (FRS).

Singaporeans who have reached the FRS are (arguably) adequately prepared for retirement.

So, really, the closure of the SA affects people who have MORE than the FRS, because they can no longer earn the 4% risk-free interest rate from their SA.

Yes, having an account that provides 4% interest, with no lock-up and no risk was a good-to-have. But I guess those days are over.

Remember, CPF is meant to serve the masses, not CPF-rich individuals.

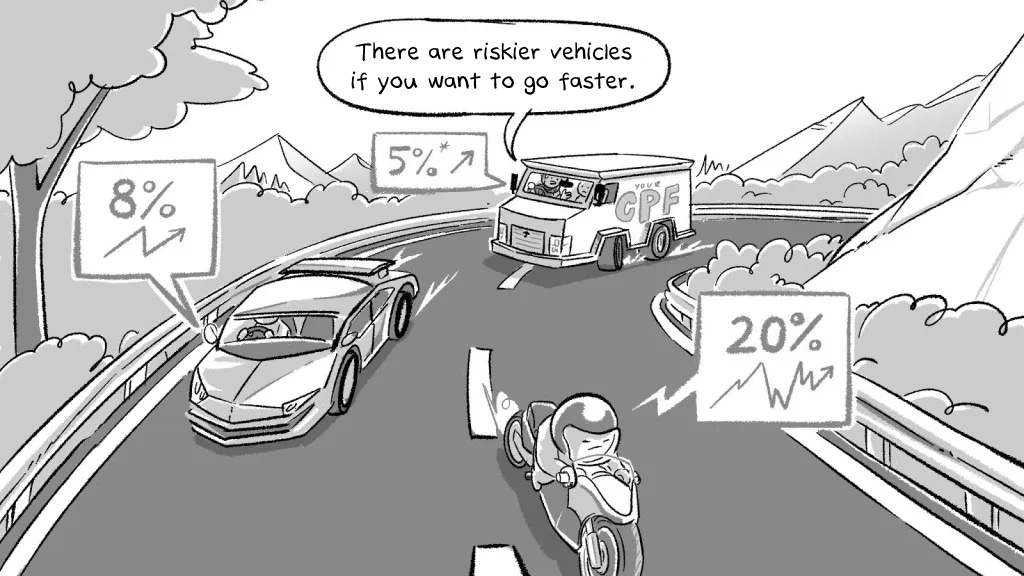

Reason 2: Solely relying on CPF has never been part of our retirement strategy.

While the CPF Special Account at 4% interest is one of the safest financial instruments available to Singaporeans, there are still risks.

We’ve always warned* people against putting too much money into their CPF accounts because:

Monies in CPF are not the most flexible in what they can be used for.

Monies in CPF tend to stay in CPF for a prolonged period of time (at least until you reach 55 years old).

Policy changes can, and have happened, depending on the government of the day as well as Singapore’s needs.

The removal of the 4% Special Account at 55 is one such example.

*We’ve warned about this here:

We like to think of CPF as one pillar of our retirement strategy, but we’re not relying on it entirely.

Reason 3: We’re still young, and so is the bulk of our target audience.

We millennials and Gen Z are still a long way from retirement. That’s plenty of time for the CPF system to change. For better or worse. We’re pretty sure this is just one change among many to come, so don’t get too hung up on it.

Besides, we see CPF as a wealth-preservation tool, not one for wealth accumulation. And at our age with years of holding power ahead of us, there are better strategies that we can use to grow our wealth, such as investing in index funds.

Most of us are still a couple decades away from turning 55. Let’s use those years wisely.

Conclusion

No conclusion, we promised y’all to keep it short.

But if you want to read more, these articles cover our approach to wealth building:

Holding power is the most underrated aspect of investing and life

The Woke Salaryman Way of Investing (up till the first 500k)

Building a globally diversified portfolio via ETFs for (idiots)

Or you can just check out all our past posts on investing here.

Here are some resources if you wanna go read up more about this topic:

CPF Board: Closure of Special Account

CPF Board (FB): Answering commons questions on the closure of SA

InvestmentMoats: Mr Lawrence Wong Woke Up on Friday Morning and Chose Violence.

Kelvin Learns Investing: CPF Shielding Is Gone Now | What You Need To Do | Budget 2024

If you’ve read this far, please consider subscribing to our email newsletter (yes, this Substack). We cannot offer you much but we can offer this:

We have newsletter-exclusive articles that won’t be posted anywhere else. We created these articles for people who want to go deeper into complex issues than the shorter-form content we typically have.

If you don’t have social media or don’t follow our Telegram channel, you can still get updates to all our content emailed directly to your inbox to read at your own time.

We promise not to spam your inbox (but Substack might, so update your notification settings).