We need to talk about why young people are overspending

We need to stop normalising $5,000 bags and $30 rides. DISCLAIMER: BROUGHT TO YOU BY MONEYSENSE AND NATIONAL YOUTH COUNCIL. DO NOT PROCEED IF YOU DO NOT LIKE SPONSORED CONTENT.

Disclaimer: This is brought to you by National Youth Council and MoneySense.

Recently, a friend shared with me that her younger sister in her early 20s was aiming to buy her first luxury bag that year. In her words, it was ‘just an entry-level bag’ costing around $5,000.

But here’s some context:

Her sister had yet to find a job and had a sizeable tuition loan to pay off, but yet intended to borrow money to make the purchase. And yes, she also did not have any emergency funds saved.

If we had to guess, this is not the first story about financial irresponsibility you’ve heard. Nor will it be the last.

While it's easy to blame young people for being financially irresponsible, I do think that there are three things that led some of them to this state.

Social media creates unrealistic expectations

Life with social media as we know it has only been around for twenty years, but to people in their 20s especially, it’s the only reality they’ve known. And here’s the thing about social media; it can cause people to have unrealistic expectations of life.

It kind of works like this:

People tend to only share the ‘highlights’ and put the best part of their day on social media

People compare their regular days to others’ life ‘highlights’

People’s best moments that they put on social media become the new normal; and it may cause some people to feel like they’re missing out on life if they aren’t able to enjoy these things

Rinse and repeat

This applies to everything from beauty standards to relationships, to happiness. And of course, the things we can afford.

Buying a luxury bag within the first year of working? Weekly catch-up with friends that cost at least $40 per pax? Ride-hailing to and from work each day? Food delivery to the office?

These aren't actually the norm, even if your social media feed shows you otherwise.

And what we often forget is:

1) The influencers who talk about their latest beauty and luxury buys every month often get these products for free, or at a huge discount

2) Those who indulge in an expensive lifestyle may come from a more privileged background

3) Even if your peers can afford a certain luxury item, it doesn’t mean that you’re on the same playing field - everyone’s spending power is different.

So many of these things that we see as ‘normal’, are actually luxuries that have been normalised.

Unsustainable business models = unrealistic expectations

In 2008, when many of our readers were still in school, something unprecedented happened in the United States and in other economies around the world.

What was it? Well, it was the start of zero interest rates implemented on an almost global scale.

This was meant to help the economy after the Global Financial Crisis, to encourage people to start spending money.

Across the world, it became incredibly cheap for businesses and investors to borrow money. Because credit was easy to access, people began taking bigger and bigger risks.

What followed was a flurry of startups prioritising speed in expanding and acquiring new customers. Instead of, you know, profitability.

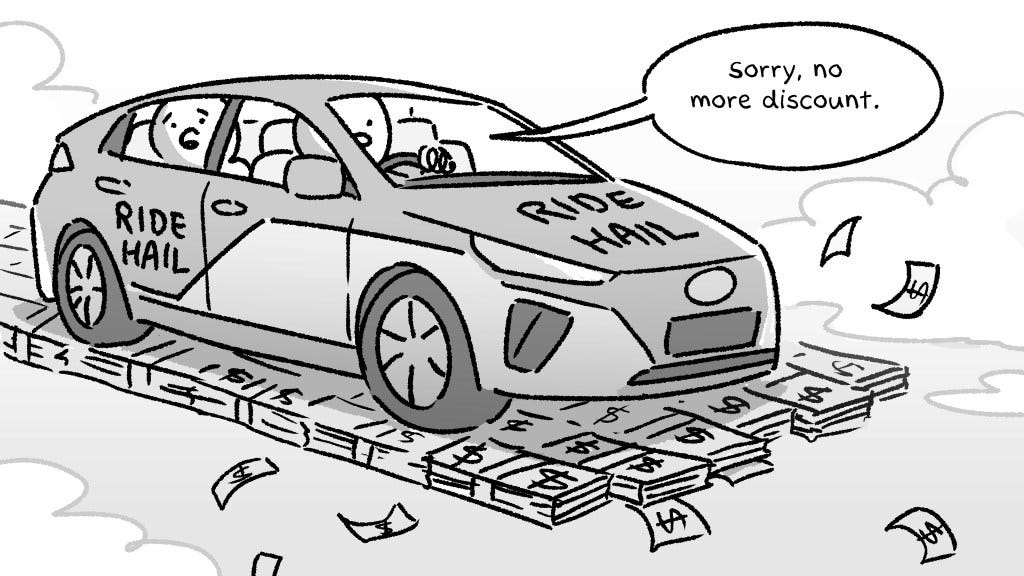

In Singapore, you might remember the years of promo codes for ride-hailing, food delivery and e-commerce.

The main idea was to get consumers used to these behaviours first, before increasing the prices at some point. Most likely after defeating their competitors.

After a few years, it worked wonderfully. Today, many young urban professionals are used to a certain level of convenience offered by these services.

But here’s the tough truth. A lot of these little conveniences were heavily subsidised. And causing massive losses for the startups and the investors involved.

But when interest rates started to rise in March 2022, companies could no longer afford to offer their services at subsidised rates.

They started increasing their prices to what they should actually have been charging to sustain their business.

And the services we’ve come to accept as normal? They’ve reverted to their true prices for business to keep going.

So if you find yourself spending a lot more on food delivery and ride-hailing than you did a few years ago, consider cutting down your reliance on these services. Prices are only going to keep increasing.

And being addicted to these conveniences is only going to put a bigger hole in your wallet.

‘Spend first, think later’ has never been easier

Don’t get us wrong.

Overspending has always been a thing.

Long before millennials were born, boomers were already spending money they didn’t have. That would be something like a big-ticket appliance – perhaps a TV – broken down into 12 months to make payments more manageable.

But what changed in between? In addition to low-interest rates that have made it easy for consumers and people to borrow money, technology has advanced.

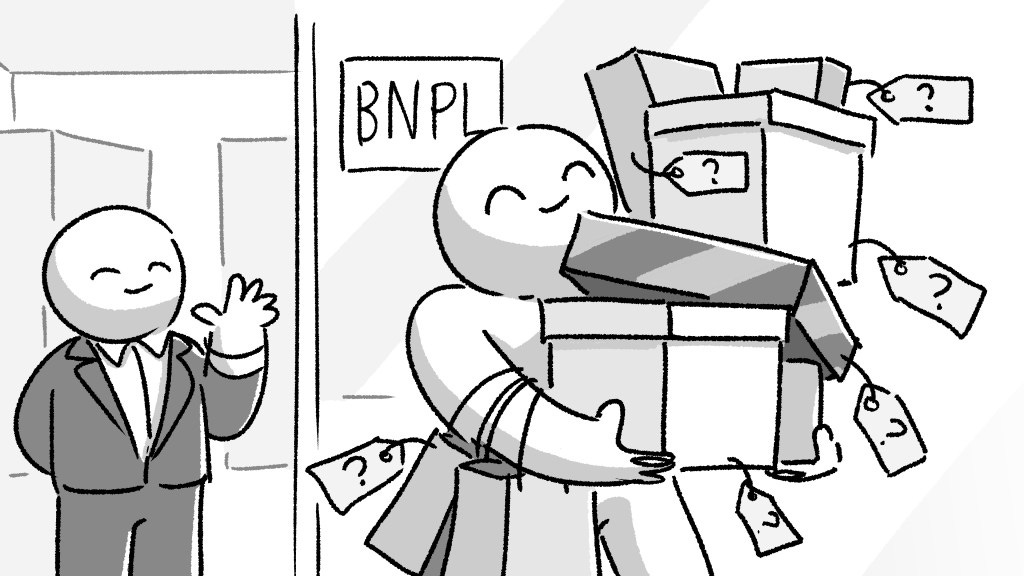

Just as how fintech has enabled micropayments, they’ve also made microloans possible. BNPL (Buy Now, Pay Later) apps is one such example.

These new fintech solutions often mean people can make instalments for just about anything these days, often without the strict income requirements needed for say, a credit card.

We’ve also seen how shops display the price you pay per instalment instead of the full price. But this also encourages impulse buying and overspending on things that one can’t afford outright.

For example: if one is considering a new luxury bag at $500 per month for 3 months, instead of a full $1,500, they may be far more tempted to buy it because parting ways with $500 is ‘less painful’.

Look, BNPL services are not inherently ’bad’ or ‘evil’. Compared to say, credit cards or other loans, BNPL democratises who can take loans. Many will say that’s a good thing.

But – this also means that they allow some of the most inexperienced and impressionable, financially illiterate people to borrow irresponsibly.

An uncertain future

Young people around the world, including in Singapore, today face multiple complex challenges, even whilst still coming out of the pandemic.

You might find some of these familiar:

Uncertainty of what the broader world will be like because of climate change and geopolitical instability.

Cost of living is rising. Concerns on housing, raising a family, medical bills and retirement have made planning for the future daunting.

Some jobs in developed countries have suffered from wage stagnation, because of global competition, AI and automation. The majority of these roles are clerical, secretarial and in manufacturing. We as creatives are also feeling the heat of our jobs being outsourced.

The prospect of looking after elderly parents who have not planned for their own retirement. You might know this as the sandwich generation.

Negative impacts on our mental health, partly due to COVID, but also today’s extremely stressful and competitive society.

More than ever, young people are faced with the choice to save up for an uncertain world or to live in the present.

But when you can’t see 20, 10 or even five years into the future, then spending all your money right now could be your way of coping with uncertainty.

What now?

To be very honest, we’re not entirely sure.

As youths ourselves, we face the same challenges as many of our millennials and Gen Z friends. And yes, we do see the appeal of living in the moment and avoiding financial responsibility.

For that reason, we are hesitant to cast judgment on young people who are spending like there’s no tomorrow – maybe in their mind, there really isn’t.

But here’s how we see it.

Short-term thinking brings fleeting happiness, but long-term suffering.

Splurging on fashion trends, holidays and the latest fads will make you happy for a while. But in the long term, financial instability and debt will mean that you will have to stop enjoying at some point.

In our opinion, it’s far better to spend responsibly – maybe even scrimp and suffer a little in the beginning – so that you can treat yourself more sustainably in the long run.

Easier said than done? You bet.

But the future is always brighter for those who can think long-term.

Stay woke, salaryman.

A message from our sponsors, National Youth Council and MoneySense

For many youths who are just stepping into the workforce and trying to navigate the corporate ladder, managing their paycheques amidst the increasing cost of living can feel stressful and daunting.

And while costs may continue rising, it does not mean that there isn’t light at the end of the tunnel; with good financial planning and budgeting, we can figure out how to manage our money consciously and carefully.

If you’re not sure where to start, consider checking out MyMoneySense, a financial planning digital service which provides a consolidated view of your finances with personalised and actionable guidance.

You could also make an appointment with a trainer from the Institute for Financial Literacy, MoneySense’s ground outreach arm, for a personalised consultation to kickstart your financial planning journey.

Whether you’re just starting work or looking to buy a home, they can provide information and guidance to help you learn how to manage your money better.

Find out more at https://www.moneysense.gov.sg/ today.